European, North American edtech startups see funding triple in 2021

Brighteye Ventures' 2021 funding report, released today, highlights key global growth and activity metrics in edtech with a focus on Europe.

Even as recently as 2019, the edtech ecosystem could have been likened to a shallow well. Funding and activity were centered in a couple of markets and there were just a few growing companies gaining interest.

But that’s no longer the case. Gone are the days when pitches to VCs would have to overcome skepticism on market size, and consumer readiness to adopt tech-enabled learning solutions.

2020 will be remembered in education circles for the tumult it caused at schools, universities and workplaces. But it will also be remembered as the year when the sector woke up to the solutions being developed by edtech companies to help people learn faster, more affordably, efficiently and effectively.

Not surprisingly, 2021 saw a boom in edtech investment across a spectra of investors. Indeed, edtech investment in 2020 and 2021 equaled the amount raised during the entire 2014-2019 period.

To carry on the initial metaphor, the edtech ecosystem is now a deep, thriving lake. Exciting companies are spawning across geographies and verticals, and even generalist investors are building conviction that the sector is capable of producing the same kind of outsized returns generated in fintech, healthtech and other sectors.

Generalist investors are taking interest in the sector due to both financial and positive impact returns, providing more competition to specialist funds.

Our 2021 funding report, released today, highlights key global growth and activity metrics in edtech with a focus on Europe. We used data primarily from Dealroom, with which we’ve developed an edtech-focused data platform.

A year of records

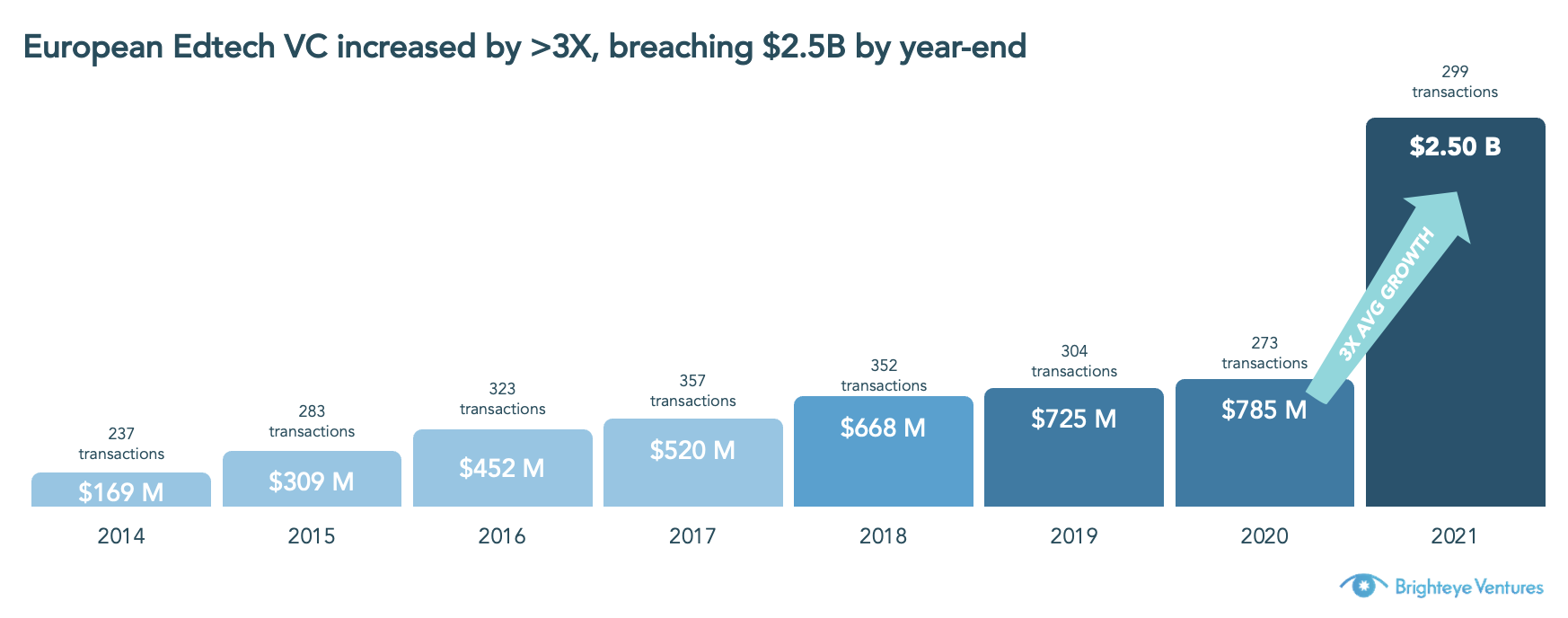

Firstly, European edtech VC investments tripled to $2.5 billion in 2021 from $790 million in 2020, compared to global funding growth of 34% to $20.1 billion in 2021 from $15 billion in 2020. The continent’s ecosystem is becoming more robust as well — the number of edtech deals in Europe accounted for 31% of all deals in the sector, up from 21% in 2019.

Image Credits: Brighteye Ventures

This growth wasn’t restricted to the usual geographies: Six European markets raised more than $100 million in 2021, compared to only one in 2020. Most of these markets are in Northern Europe, so we hope, and expect, to see some major players breaking out in Southern Europe in 2022 (particularly in Spain, Portugal and Italy).